ICT-IOT

Edtech Market

Edtech Market Size, Share, Growth & Industry Analysis, By Deployment (Cloud, On-Premise), By Application (K-12, Higher Education, Others), By Type (Hardware, Software) and Regional Analysis, 2024-2031

Pages : 120

Base Year : 2023

Release : May 2024

Report ID: KR722

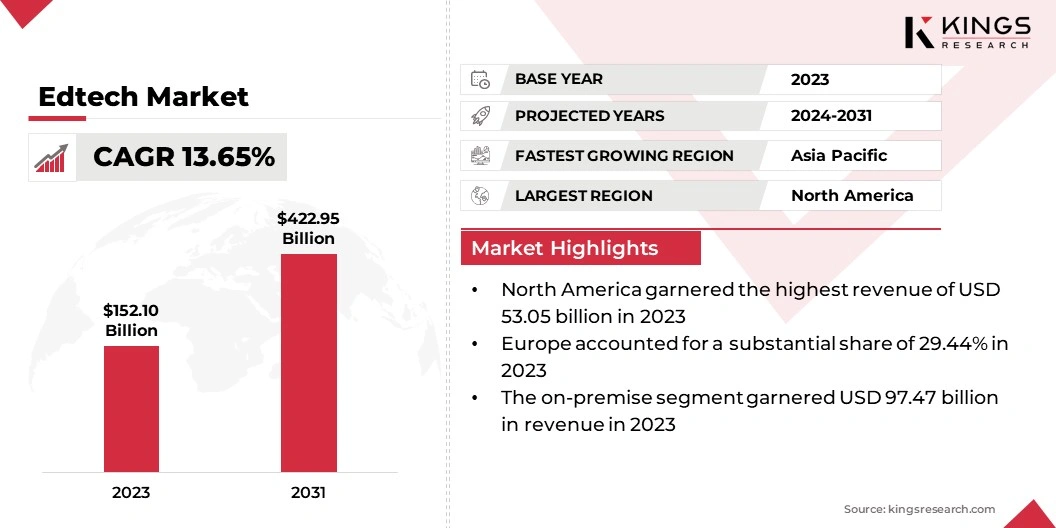

Edtech Market Size

Global Edtech Market size was recorded at USD 152.10 billion in 2023, which is estimated to be at USD 172.71 billion in 2024 and projected to reach USD 422.95 billion by 2031, growing at a CAGR of 13.65% from 2024 to 2031. Globalization and the increasing demand for education beyond traditional classrooms are contributing to market growth. In the scope of work, the report includes solutions offered by companies such as Anthology Inc., Coursera Inc., Udemy, Inc., McGraw Hill, Duolingo, Inc., Showbie Inc., FutureLearn Limited, BYJU'S, upGrad Education Private Limited, Edutech, and others. With economies becoming increasingly interconnected and industries evolving, there is a growing emphasis on lifelong learning and upskilling to remain competitive in the job market.

This has led to the proliferation of online learning platforms, offering a diverse range of courses and certifications tailored to the needs of learners worldwide. Furthermore, the COVID-19 pandemic boosted the adoption of remote learning solutions, highlighting the importance of flexible and accessible education delivery models.

This shift toward online education has offered new opportunities for edtech companies to expand their market reach and cater to diverse learner demographics, including working professionals, adult learners, and students in urban and remote locations. Moreover, the rise of international student mobility has fueled the demand for digital learning solutions that transcend geographical boundaries, enabling seamless access to educational resources and fostering cross-cultural exchange.

The global edtech market encompasses the provision of technological solutions and platforms designed to enhance and facilitate educational processes, both formal and informal, across various levels of learning. It includes a wide range of products and services such as online learning platforms, educational apps, learning management systems (LMS), virtual classrooms, digital content, and adaptive learning software.

Edtech solutions leverage advanced technologies such as artificial intelligence, machine learning, augmented reality, and mobile applications to personalize learning experiences, improve academic outcomes, and provide access to education anytime, anywhere. This dynamic market caters to students, educators, institutions, corporations, and lifelong learners, fostering innovation and transformation in the education sector.

Analyst’s Review

The global edtech market is poised to witness robust growth, propelled by factors such as increasing digitization of education, rising demand for personalized learning solutions, expanding internet penetration, and the growing adoption of mobile learning devices. Key players in the industry are prioritizing innovation, developing scalable and adaptable platforms, forging strategic partnerships with educational institutions, leveraging data analytics to drive personalized learning experiences, and focusing on user-centric design to enhance accessibility and usability. Moreover, to maintain competitiveness and market leadership in this rapidly evolving landscape, companies are shifting toward subscription-based models, investing in content development, and expanding into emerging markets.

Edtech Market Growth Factors

The COVID-19 pandemic has contributed to the shift toward online learning and underscored its significance, with flexibility and accessibility emerging as paramount factors. This surge in demand for online education has persisted beyond the pandemic, propelling the demand for remote learning solutions such as online courses and tutoring platforms.

Moreover, the notable shift toward personalized learning experiences, facilitated by edtech tools leveraging AI and big data, is propelling market expansion. Recognizing the limitations of traditional, one-size-fits-all education, these solutions offer tailored learning paths, adaptive content delivery, and customized teaching approaches. By catering to individual learning styles and preferences, personalized learning enhances student engagement and academic outcomes, thereby increasing the adoption of edtech solutions.

Furthermore, the rapid pace of automation and technological advancements is reshaping the job market, thereby necessitating a continuous commitment to upskilling and reskilling the workforce. This imperative for lifelong learning is driving demand for edtech solutions in corporate training, professional certifications, and micro-learning platforms. As individuals seek to remain competitive in a rapidly evolving landscape, edtech companies are poised to capitalize on the growing need for accessible, on-demand learning opportunities tailored to the changing demands of the modern workforce.

However, the digital divide and infrastructure issues pose significant challenges to the widespread adoption of educational technology. In regions with limited internet access and device availability, consumers face barriers to accessing online learning resources, thus exacerbating educational inequalities. For instance, rural areas or developing countries often lack the necessary infrastructure for seamless edtech integration, thereby hindering educational progress.

Additionally, data privacy presents a significant concern in the edtech landscape. While personalized learning relies on student data, key players are focusing on ensuring privacy and security. Companies are implementing transparent data practices and robust security measures to mitigate these concerns, which is fostering trust among educators, students, and parents while enabling responsible use of edtech solutions.

Edtech Market Trends

Mobile learning platforms are experiencing a surge in popularity, fueled by the widespread adoption of smartphones and tablets. These devices offer students unprecedented access to educational resources on the go, thereby eliminating constraints related to time and location. For instance, language learning apps leverage mobile technology to provide interactive lessons and real-time feedback, empowering learners to practice anytime, anywhere.

Moreover, artificial intelligence (AI) is revolutionizing education by personalizing learning experiences and streamlining administrative tasks. AI-powered adaptive learning systems analyze student data to tailor content delivery, which ensures individualized learning paths. Moreover, AI-driven content creation tools automate the development of interactive course materials, thereby enhancing efficiency and scalability. Intelligent tutoring systems offer personalized support and feedback, replicating the benefits of one-on-one instruction.

Moreover, edtech solution advancing with a focus on soft skills development. Recognizing the importance of skills such as critical thinking, communication, and problem-solving, edtech platforms offer interactive simulations, collaborative projects, and gamified learning experiences. For instance, virtual reality (VR) simulations enable students to practice problem-solving and decision-making in realistic scenarios, which fosters skill acquisition in a safe and immersive environment. By leveraging mobile technology, AI, and a focus on soft skills, the market is poised to transform education and empower learners for success in the digital age.

Segmentation Analysis

The global edtech market is segmented based on deployment, application, type, and geography.

By Deployment

Based on deployment, the market is bifurcated into cloud and on-premise. The on-premise segment garnered the highest revenue of USD 97.47 billion in 2023. On-premise solutions are tailored to meet the needs of certain market segments, such as large enterprises or institutions with specific security or data privacy requirements.

For instance, educational institutions handling sensitive student data prefer on-premise solutions to maintain greater control and security over their data. Additionally, regulatory compliance mandates in certain industries or regions necessitate the use of on-premise deployments. Furthermore, legacy systems and infrastructure limitations are contributing to the rising demand for on-premise solutions among certain organizations.

By Application

Based on application, the market is categorized into K-12, higher education, and others. The K-12 segment captured the largest market share of 42.81% in 2023. The K-12 education sector represents a substantial demographic comprising numerous students, teachers, and educational institutions, which is contributing to the demand for a wide range of edtech solutions tailored to meet the diverse needs of K-12 learners. Factors such as government initiatives to modernize K-12 education, increasing digital literacy among students and educators, and the integration of technology into curriculum standards are playing a pivotal role in driving the adoption of edtech solutions.

Additionally, the growing emphasis on personalized learning approaches and the need to address educational inequalities fuel the demand for innovative edtech solutions in the K-12 sector, thereby stimulating the growth of the segment.

By Type

Based on type, the market is divided into hardware and software. The software segment is anticipated to witness the highest growth at a CAGR of 14.08% over 2024-2031. Software solutions offer flexibility, scalability, and ease of integration, catering to the evolving needs of educational institutions and learners. Factors such as the increasing adoption of cloud-based software-as-a-service (SaaS) models, the proliferation of mobile learning applications, and the demand for AI-driven personalized learning platforms are contributing to the robust growth of the software segment.

Moreover, software solutions often require lower initial investment compared to hardware, making them more accessible to a broader range of users, including small and medium-sized educational institutions and individual learners.

Edtech Market Regional Analysis

Based on region, the global edtech market is classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

North America garnered the highest revenue of USD 53.05 billion in 2023. The region presents a dynamic landscape for edtech innovation, driven by a strong emphasis on STEM education. Edtech solutions leveraging virtual reality (VR), augmented reality (AR), and interactive tools are poised to enhance learning experiences. For instance, VR simulations allow students to explore complex scientific concepts in a hands-on manner, thereby fostering deeper understanding and engagement in STEM subjects.

Moreover, the region's robust venture capital ecosystem and culture of innovation are leading to significant investment in the market. This environment is attracting both startups and established players, which is supporting the development of cutting-edge educational technologies. Major universities offering online degrees and established online learning platforms are contributing to the region's readiness for digital education solutions. Within this landscape, the implementation of personalized learning on a large scale emerges as a key opportunity.

Europe accounted for a substantial share of 29.44% in 2023. The region's educational technology landscape is shaped by a rising focus on equity and inclusion. Edtech solutions tailored to address the needs of students with disabilities and those from marginalized backgrounds hold significant promise in fostering educational equality. Additionally, the multilingual landscape in Europe presents opportunities for edtech companies to develop innovative language learning solutions.

Moreover, stringent data protection regulations in the region, such as GDPR, are fostering trust in the edtech sector by prioritizing user privacy. Responsible data practices build confidence among parents and educators, thereby supporting the widespread adoption of digital learning solutions. Edtech has the potential to flourish within this regulatory environment, particularly by supporting vocational training programs and apprenticeships. These programs are essential for developing a skilled workforce across Europe.

Competitive Landscape

The global edtech market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions. Companies are implementing several strategic initiatives, such as expanding services, investing in research and development (R&D), establishing new service delivery centers, and optimizing their service delivery processes, which are likely to create new opportunities for market growth.

List of Key Companies in Edtech Market

- Anthology Inc.

- Coursera Inc.

- Udemy, Inc.

- McGraw Hill

- Duolingo, Inc.

- Showbie Inc.

- FutureLearn Limited

- BYJU’S

- upGrad Education Private Limited

- Edutech

Key Industry Developments

- March 2023 (Acquisition): LEAD acquired the K-12 learning business of Pearson, a London Stock Exchange-listed education group, in India. This acquisition facilitated the startup's expansion, reaching 5 million students nationwide. LEAD stated in a release that the acquisition of Pearson India's local K-12 learning business positions them to offer integrated edtech solutions to over 60,000 schools across India by 2026.

The Global Edtech Market is Segmented as:

By Deployment

- Cloud

- On-Premise

By Application

- K-12

- Higher Education

- Others

By Type

- Hardware

- Software

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

CHOOSE LICENCE TYPE

Frequently Asked Questions (FAQ's)

Get the latest!

Get actionable strategies to empower your business and market domination

- Deliver Revenue Impact

- Demand Supply Patterns

- Market Estimation

- Real-Time Insights

- Market Intelligence

- Lucrative Growth Opportunities

- Micro & Macro Economic Factors

- Futuristic Market Solutions

- Revenue-Driven Results

- Innovative Thought Leadership