Electrostatic Precipitator Market

Electrostatic Precipitator Market Size, Share, Growth & Industry Analysis, By System (Dry, Wet), By Application (Chemical, Metal, Power Generation, Cement, Manufacturing, Others), and Regional Analysis, 2024-2031

Pages : 120

Base Year : 2023

Release : August 2024

Report ID: KR982

Electrostatic Precipitator Market Size

The global Electrostatic Precipitator Market size was valued at USD 8.02 billion in 2023 and is projected to grow from USD 8.27 billion in 2024 to USD 11.06 billion by 2031, exhibiting a CAGR of 4.23% during the forecast period. The rapid growth of industrialization leads to increased air pollution, thereby boosting the demand for electrostatic precipitators. Moreover, stricter regulations are promoting the use of electrostatic precipitators to meet air quality standards.

In the scope of work, the report includes products offered by companies such as Bedcock & Wilcox, FLSmidth, DUCON, General Electric, John Wood Group plc, Mitsubishi Power Ltd., Hamon, Siemens AG, Thermax Ltd., Trion IAQ, and others.

Stricter global air quality regulations are propelling the growth of the electrostatic precipitator market, ensuring that industries comply with evolving environmental standards. As industrial activities increase, the corresponding rise in emissions necessitates the implementation of effective pollution control measures.

- The 29th edition of the International Yearbook of Industrial Statistics 2023 reported a global growth of 2.3% in the industrial sector, primarily fueled by a 3.2% increase in manufacturing, while the combined mining and utilities sector experienced a contraction of 0.9%.

Electrostatic precipitators, known for their efficiency in particulate matter removal, are being increasingly adopted to mitigate environmental impact and adhere to regulatory requirements. This trend underscores the critical role of advanced pollution control technologies in maintaining air quality and supporting sustainable industrial practices.

Electrostatic precipitators (ESPs) are devices specifically designed to remove fine particles, including dust and smoke, from gas streams. They work by charging particles in the air, which are then attracted to and adhere to oppositely charged plates, effectively capturing and removing them from the air. ESPs are widely used across diverse industries such as power generation, manufacturing, and mining to control emissions and improve air quality.

Their applications include capturing harmful particulate matter from exhaust gases, ensuring compliance with environmental regulations, and enhancing overall operational efficiency. By reducing air pollution, electrostatic precipitators contribute to a healthier environment and support sustainability initiatives across various sectors.

Analyst’s Review

The global electrostatic precipitator market is evolving due to increased regulatory pressures and environmental concerns. Prominent players are increasing their investment in R&D to reduce emissions.

- For instance, the European Commission's Joint Research Centre (JRC) reported that Europe’s top companies invested over USD 1,349.06 billion in R&D in 2023, with a particular focus on green technologies to enhance sustainability.

In the U.S., substantial resources have been allocated to advancing energy innovation, with particular investments in carbon capture, hydrogen, and advanced nuclear energy technologies. This allocation underscores a strong commitment to decarbonizing industrial processes and achieving net-zero emissions.

- In April 2024, Clyde Industries Brazil conducted a final quality inspection at EETC Bengbu Factory as part of an Electrostatic Precipitator retrofit project. This inspection highlights the company's ongoing efforts to improve emission control systems.

Prioritizing product innovation is a key imperative for electrostatic precipitator manufacturers to succeed in the market. Investing in R&D of advanced technologies, such as carbon capture and hydrogen, is crucial.

- According to the World Bank, in 2023, global carbon pricing revenues reached a record USD 104 billion, with 75 carbon pricing instruments currently in operation worldwide. This indicates a growing commitment to reducing carbon emissions through economic measures

Emphasizing compliance with stringent environmental regulations helps safeguard against potential legislative changes, thereby ensuring long-term compliance and stability. Additionally, expanding into emerging markets with rising industrial activities and environmental concerns aids in diversifying revenue streams.

Offering tailored solutions and services, such as customized maintenance packages and real-time monitoring systems, are crucial in enhancing customer satisfaction and fostering loyalty.

Electrostatic Precipitator Market Growth Factors

Rapid urbanization is propelling the growth of the global electrostatic precipitator market. As pollution levels in cities increase, the demand for advanced air filtration systems is anticipated to rise significantly.

- According to the United Nations, Department of Economic and Social Affairs, 68% of the world's population is anticipated to reside in urban areas by 2050. This shift is projected to substantially increase the demand for effective pollution control measures.

Global sustainability initiatives are leading to increased adoption of electrostatic precipitators across various sectors. The European Green Deal, which targets achieving net-zero emissions by 2050, is catalyzing substantial investments in green technologies. Increasing industrial activities contribute to higher emissions, highlighting the need for efficient pollution control solutions.

Stringent environmental regulations worldwide are boosting the demand for electrostatic precipitators, as industries seek to comply with evolving standards. Additionally, growing public awareness about the health impacts of air pollution is prompting industries to adopt cleaner technologies, thereby propelling the growth of the electrostatic precipitator market.

- According to the National Institute of Environmental Health Sciences, U.S., air pollution is responsible for over 6.5 million deaths annually worldwide. This highlights the critical need for effective air quality management and advanced pollution control technologies

However, the substantial upfront investment required for electrostatic precipitators is deterring potential buyers in developing markets, where financial constraints are considerable. Additionally, ongoing maintenance and operational costs add to the overall expenditure. The emergence of alternative emission control technologies, such as fabric filters and catalytic converters, presents a substantial threat.

To mitigate these challenges, key players in the market are focusing on reducing costs through technological advancements aimed at enhancing efficiency and lowering production expenses. Offering financing options or leasing models helps ease the burden of high initial costs.

Additionally, manufacturers are investing heavily in integrating features that reduce maintenance needs and enhance performance, thereby increasing the competitiveness of electrostatic precipitators compared to alternative technologies.

Electrostatic Precipitator Market Trends

Technological advancements are transforming the electrostatic precipitator market by enhancing efficiency and reducing costs. Innovations such as hybrid systems, which combine ESPs with fabric filters or other emission control technologies, are improving performance and operational efficiency. These hybrid systems leverage the strengths of both technologies, leading to improved particulate collection and lower overall costs.

Additionally, a growing emphasis on energy efficiency is reshaping the market. Manufacturers are developing ESPs that are designed to consume less energy, thus reducing operational costs and minimizing the environmental impact. This focus on energy efficiency aligns with global trends toward sustainability and cost-effectiveness.

Moreover, retrofitting and upgrading existing ESP systems have become a priority for numerous industries. Rather than investing in new installations, companies are opting to update their current systems to meet stringent regulations and enhance performance. This approach ensures compliance with evolving standards and extends the lifespan of existing equipment, making it a cost-effective solution for many industries.

Segmentation Analysis

The global market is segmented based on system, application, and geography.

By System

Based on system, the market is bifurcated into dry and wet. The dry segment led the electrostatic precipitator market in 2023, reaching a valuation of USD 6.48 billion. Dry ESPs are highly preferred due to their lower operational costs and simpler maintenance compared to wet systems. They are particularly effective in industries where the collected dust is dry and manageable, such as in cement and coal-fired power plants.

Their efficiency in removing particulates, combined with a reduced need for water and chemical handling, further contributes to their cost-effectiveness. Additionally, the lower installation and operational costs of dry ESP make it a more attractive option for numerous industries, thereby reinforcing its dominant market position.

By Application

Based on application, the market is classified into chemical, metal, power generation, cement, manufacturing, and others. The power generation segment secured the largest revenue share of 39.79% in 2023. Power plants, especially those that utilize coal as fuel, produce significant amounts of dust and particulate matter, making effective emission control essential.

Electrostatic precipitators are highly effective in capturing these particulates, thereby ensuring compliance with stringent environmental regulations. Their ability to handle large volumes of flue gas and high dust loads makes them particularly suitable for power generation facilities. Additionally, as power plants seek to reduce their environmental footprint and improve operational efficiency, there is a growing demand for advanced ESP solutions in this sector.

Electrostatic Precipitator Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

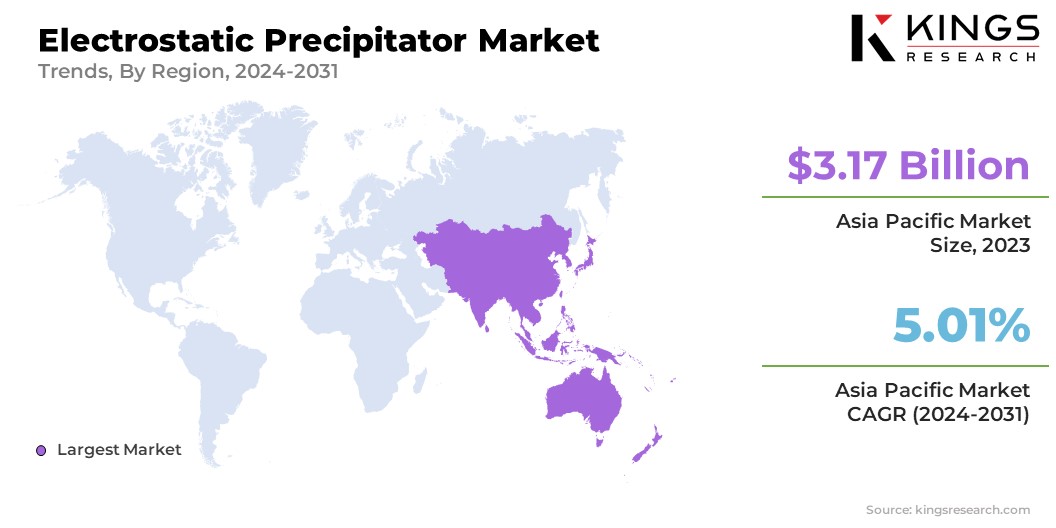

Asia Pacific electrostatic precipitator market share stood around 39.53% in 2023 in the global market, with a valuation of USD 3.17 billion. The region’s dominance is attributed to rapid industrialization, growing energy demands, and stringent environmental regulations in countries such as China and Japan. The region's robust manufacturing and power generation sectors are boosting the demand for efficient emission control solutions.

- According to the 2023 EU industrial R&D investment scoreboard, in 2000, 84.1% of patents were filed by high-income industrial economies. By 2022, however, middle-income industrial economies, particularly those in Asia, accounted for 54.3% of patent filings.

This shift indicates a strong innovation and manufacturing base in these regions, which support the advancement of ESP technologies. The increasing focus on environmental compliance and technological advancements further solidifies Asia Pacific's leading position in the market.

North America is poised to witness significant growth at a robust CAGR of 4.36% over the forecast period. This growth is mainly fostered by stringent environmental regulations and a strong emphasis on reducing industrial emissions, particularly in the power generation and manufacturing sectors.

Additionally, the region's advanced infrastructure and technological capabilities support the adoption of cutting-edge ESP technologies. The ongoing investment in upgrading existing systems to meet evolving standards and a strong emphasis on energy efficiency further boost regional market expansion. The region’s commitment to sustainability and regulatory compliance, along with its innovative industrial practices, highlights the anticipated growth of the market.

Competitive Landscape

The global electrostatic precipitator market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Strategic initiatives, including investments in R&D activities, the establishment of new manufacturing facilities, and supply chain optimization, could create new opportunities for market growth.

List of Key Companies in Electrostatic Precipitator Market

- Bedcock & Wilcox

- FLSmidth

- DUCON

- General Electric

- John Wood Group plc

- Mitsubishi Power Ltd.

- Hamon, Siemens AG

- Thermax Ltd.

- Trion IAQ

Key Industry Developments

- January 2024 (Acquisition): Babcock & Wilcox (B&W) enhanced its environmental solutions by acquiring Hamon Research-Cottrell's emissions control technologies. This addition strengthened B&W's portfolio of advanced air quality control systems, providing customers with improved options for reducing emissions. The strategic move aimed to advance sustainability efforts across various industries, further reinforcing B&W's commitment to cleaner energy solutions.

- September 2023 (Technological Advancement): Valmet announced its plans to supply an electrostatic precipitator (ESP) for Shandong Huatai Paper's 700,000-tonne chemical pulp project in Shandong, China. The delivery is scheduled for January 2025. This initiative is part of Huatai’s commitment to sustainability, focusing on reducing emissions and achieving low energy consumption and zero pollution.

The global electrostatic precipitator market is segmented as:

By System

- Dry

- Wet

By Application

- Chemical

- Metal

- Power Generation

- Cement

- Manufacturing

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

CHOOSE LICENCE TYPE

.webp)

Frequently Asked Questions (FAQ's)

Get the latest!

Get actionable strategies to empower your business and market domination

- Deliver Revenue Impact

- Demand Supply Patterns

- Market Estimation

- Real-Time Insights

- Market Intelligence

- Lucrative Growth Opportunities

- Micro & Macro Economic Factors

- Futuristic Market Solutions

- Revenue-Driven Results

- Innovative Thought Leadership