Market Definition

The market comprises the production, distribution, and consumption of petroleum-based fuels, including gasoline, diesel, and aviation fuel, for transportation purposes.

This market involves key stakeholders such as oil producers, refineries, and fuel retailers, with its dynamics influenced by factors such as crude oil prices, regulatory policies, and the transition to alternative energy sources. Environmental regulations and technological advancements are further shaping the industry's development and sustainability.

Oil Fuel Mobility Market Overview

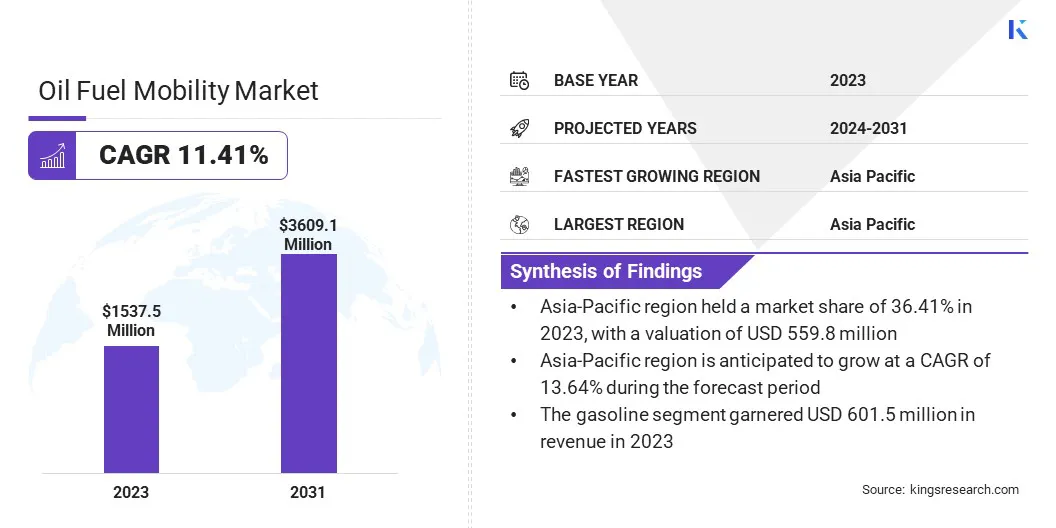

Global oil fuel mobility market size was valued at USD 1,537.53 million in 2023 and is projected to grow from USD 1,693.68 million in 2024 to USD 3,609.16 million by 2031, exhibiting a CAGR of 11.41% during the forecast period.

The oil fuel market is a critical component of the global transportation and energy sectors, supplying fuel for automobiles, aviation, and maritime industries. Despite the increasing adoption of alternative energy sources, petroleum-based fuels continue to dominate due to their high energy density, cost efficiency, and well-established infrastructure. Market growth is fueled by rising transportation demand, industrial expansion, and global trade.

Major companies operating in the oil fuel mobility industry are Saudi Arabian Oil Co., China Petrochemical Corporation, Royal Dutch Shell Plc.com, Exxon Mobil Corporation, Chevron Corporation, BP p.l.c., Marathon Petroleum Corporation, Phillips 66 Company, Indian Oil Corporation Ltd, TotalEnergies, PetroChina Company Limited, LUKOIL, Marathon Petroleum Corporation, Repsol, Eni S.p.A., and others.

- In June 2023, U.S. Oil and U.S. Gain merged to form U.S. Energy, a vertically integrated energy solutions provider. The new entity offers refined products, alternative fuels, and environmental credits, leveraging a broad asset portfolio that includes fuel terminals, renewable projects, and alternative fuel stations. S. Energy focuses on enhancing sustainability and operational efficiency while addressing diverse transportation energy needs.

Key Highlights:

- The oil fuel mobility industry size was recorded at USD 1,537.53 million in 2023.

- The market is projected to grow at a CAGR of 11.41% from 2024 to 2031.

- Asia-Pacific held a share of 36.41% in 2023, valued at USD 559.81 million.

- The commercial vehicle segment is expected to reach USD 1,330.84 million by 2031.

- The gasoline segment garnered USD 601.48 million in revenue in 2023.

- The commercial fleets segment is anticipated to witness the fastest CAGR of 12.81% over the forecast period.

- Asia Pacific is estimated to grow at a CAGR of 13.64% through the projection period.

How are growing logistics networks driving the demand for this market?

The growing number of vehicles, expanding commercial transport operations, and rising air travel globally continue to drive the demand for petroleum-based fuels, supporting the growth of the oil fuel mobility market.

Factors such as rapid urbanization, the expansion of logistics networks, and overall economic growth contribute to increased fuel consumption across the automotive, aviation, and shipping sectors. Emerging economies with expanding middle-class populations are witnessing higher rates of vehicle ownership, further stimulating demand.

Despite the advancement of alternative energy sources, oil-based fuels remain the primary choice for mobility due to their high energy density, well-established infrastructure, and cost-effectiveness.

- In December 2023, VARO Energy and Höegh Autoliners partnered to accelerate sustainable shipping by supplying 100% advanced biofuels, reducing greenhouse gas emissions by 85% compared to conventional maritime fuels. This collaboration supports decarbonization efforts in deep-sea shipping and aligns with international climate goals. The partnership highlights the role of biofuels in reducing emissions while maintaining operational efficiency.

How is oil price volatility slowing market growth?

The volatility of crude oil prices poses a major challenge to the progress of the oil fuel mobility market, impacting fuel costs, profitability, and market stability. Prices fluctuate due to geopolitical tensions, OPEC policies, economic conditions, and external factors such as natural disasters and currency fluctuations.

These uncertainties make long-term planning difficult for fuel suppliers, transportation companies, and consumers.

To mitigate these risks, industry stakeholders are adopting price management strategies and investing in alternative energy sources such as biofuels, hydrogen, and electric mobility to reduce reliance on oil. Strategic petroleum reserves ensure supply stability, while efficient supply chains and long-term contracts minimize cost uncertainties.

Hedging strategies mitigate price risks, and policy measures such as fuel subsidies or tax adjustments provide consumer relief. Advancements in fuel efficiency and refining technologies enhance cost-effectiveness and reduce long-term market exposure.

How is transition towards alternative fuels affecting the market?

The transition to alternative fuels is emerging as a significant trend in the oil fuel mobility market, aided by environmental regulations, government policies, and advancements in clean energy technologies.

Increasingly stringent carbon emission standards and fuel efficiency requirements are prompting industries to reduce dependence on petroleum-based fuels. Governments and corporations are investing substantially in biofuels, hydrogen, and synthetic fuels, while the growing adoption of electric vehicles (EVs) is increasing fuel demand.

Furthermore, advancements in carbon capture and storage (CCS) technologies and the development of sustainable aviation and marine fuels are accelerating this shift.

- In July 2023, BP invested $10 million in WasteFuel, a U.S.-based biofuels company, to expand its bioenergy portfolio. WasteFuel is developing a global network of plants that convert municipal and agricultural waste into bio-methanol, a low-carbon fuel for shipping. This investment aligns with BP’s strategy to support decarbonization efforts in hard-to-abate sectors. The partnership includes an agreement for BP to offtake bio-methanol and collaborate on improving production efficiency.

Oil Fuel Mobility Market Report Snapshot

|

Segmentation

|

Details

|

|

By Vehicle Type

|

Passenger Cars, Commercial Vehicles, Two-Wheelers, Others (off-road vehicles, construction equipment, and other specialized vehicles)

|

|

By Fuel Type

|

Gasoline, Diesel, Compressed Natural Gas (CNG), Others (Liquefied Petroleum Gas (LPG), Biodiesel)

|

|

By End User

|

Individual Consumers, Public Transportation, Commercial Fleets, Government and Municipalities

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, U.K., Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, UAE, Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation:

- By Vehicle Type (Passenger Cars, Commercial Vehicles, Two-Wheelers, and Others (off-road vehicles, construction equipment, and other specialized vehicles)): The passenger car segment earned USD 585.79 million in 2023, mainly due to rising demand for private vehicle ownership, increasing disposable income, and rapid urbanization.

- By Fuel Type (Gasoline, Diesel, Compressed Natural Gas (CNG), and Others (Liquefied Petroleum Gas (LPG), Biodiesel)): The gasoline segment held a share of 39.12% in 2023, largely attributed to its widespread availability, affordability, and dominance in passenger vehicles.

- By End User (Individual Consumers, Public Transportation, Commercial Fleets, and Government and Municipalities): The individual consumers segment is projected to reach USD 1,538.54 billion by 2031, propelled by the rising demand for personal mobility due to urban expansion and improving road infrastructure.

What is the market scenario in North America and Asia-Pacific region?

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

Asia Pacific oil fuel mobility market captured a substantial share of around 36.41% in 2023, valued at USD 559.81 million. This leading position is strengthened by strong industrialization, expanding logistics and transportation sectors, and a surge in ride-hailing services. The increasing demand for commercial fleets, including trucks and buses, has significantly contributed to fuel consumption across the region.

Ongoing infrastructure projects and cross-border trade activities have highlighted the need for efficient fuel mobility solutions. Despite the rising interest in alternative energy sources, conventional fuels continue to dominate due to their cost-effectiveness and well-established supply chains.

Ongoing infrastructure projects and cross-border trade activities have highlighted the need for efficient fuel mobility solutions. Despite the rising interest in alternative energy sources, conventional fuels continue to dominate due to their cost-effectiveness and well-established supply chains.

- In February 2025, ONGC completed the acquisition of Ayana Renewable Power Private Limited, reinforcing its commitment to clean energy investments. This strategic move aligns with ONGC’s long-term sustainability goals and India's renewable energy transition. The acquisition enhances ONGC’s renewable energy portfolio by leveraging Ayana’s expertise in solar and wind power generation. By integrating renewable assets, ONGC aims to diversify its energy mix and support the country’s net-zero ambitions.

North America oil fuel mobility industry is set to grow at a CAGR of 9.59% over the forecast period, propelled by increasing transportation fuel demand, advancements in refining technologies, and strategic investments in biofuels and carbon capture solutions. The regional market benefits from strong infrastructure, government incentives, and a growing shift toward sustainable fuel alternatives.

Key industry players are expanding their operations and adopting innovative solutions to enhance fuel efficiency and reduce emissions, ensuring long-term regional market expansion.

- In October 2023, Chevron announced an agreement to acquire Hess Corporation in an all-stock transaction valued at $53 billion. This acquisition enhances Chevron’s asset portfolio, particularly with Hess’ holdings in Guyana and the Bakken shale. The deal is expected to strengthen production growth, free cash flow, and shareholder returns.

Regulatory Framework

- In India, the Petroleum and Natural Gas Regulatory Board (PNGRB) is responsible for overseeing oil and gas regulations. The FIPI guidelines provide a framework for regulatory policies, covering areas such as entity selection, storage capacity, pipeline operations, marketing obligations, and transportation tariffs. The document also examines existing Indian regulations, industry perspectives, and international best practices, aiming to establish a transparent and efficient regulatory system under the PNGRB Act 2006.

- The Government of Canada has established a regulatory framework to cap and reduce greenhouse gas (GHG) emissions from the oil and gas sector to achieve net-zero emissions by 2050. Implemented under the Canadian Environmental Protection Act, 1999 (CEPA), the plan includes a national cap-and-trade system to ensure emissions reductions while maintaining economic competitiveness.

- The European Commission's Fuel Quality Directive sets strict standards for road transport fuels in the EU to protect health and the environment while ensuring fuel compatibility across countries. It regulates emissions, fuel composition, and blending limits for biofuels.

- In the U.S., the Federal Energy Regulatory Commission (FERC) regulates interstate oil pipeline transportation. It oversees pipeline rates, and tariffs, and ensures non-discriminatory access. While it does not regulate oil production or local distribution, FERC ensures fair pricing and transparent market operations.

- The U.S. Department of Energy (DOE) regulates the import and export of natural gas and liquefied natural gas (LNG) under the Natural Gas Act (NGA). Companies must obtain authorization before engaging in cross-border gas transactions. Applications must be filed at least 90 days in advance and follow DOE’s procedural guidelines.

Competitive Landscape

The oil fuel mobility market is characterized by a number of participants, including both established corporations and emerging players. To gain a competitive edge, companies are focusing on strategic initiatives such as mergers, acquisitions, and partnerships. They are further exploring diversification strategies, such as venturing into renewable energy sectors, to reduce reliance on traditional fuel sources.

Regulatory compliance remains a priority, boosting the adoption of cleaner production methods. Additionally, market participants leverage data analytics and AI-driven solutions to optimize fuel distribution and consumption patterns, enhancing operational efficiency.

- In January 2025, Aramco signed 145 agreements and MoUs worth $9 billion at the iktva Forum & Exhibition, reinforcing supply chain resilience and localization efforts. Key developments included the launch of ASMO, a joint venture with DHL, and the inauguration of two strategic manufacturing facilities. Aramco’s iktva score rose to 67% in 2024 from 35% in 2015, highlighting significant progress in local procurement. The program aims to reach 70% localization, boost exports, and create job opportunities.

List of Key Companies in Oil Fuel Mobility Market:

- Saudi Arabian Oil Co.

- China Petrochemical Corporation

- Royal Dutch Shell Plc .com

- Exxon Mobil Corporation

- Chevron Corporation

- BP p.l.c.

- Marathon Petroleum Corporation

- Phillips 66 Company

- Indian Oil Corporation Ltd

- TotalEnergies

- PetroChina Company Limited

- LUKOIL

- Marathon Petroleum Corporation

- Repsol

- Eni S.p.A.

Recent Developments (M&A/Partnerships/Agreements/New Product Launch)

- In December 2024, Aramco completed the acquisition of a 10% equity stake in Horse Powertrain Limited, a leader in hybrid and internal combustion powertrain solutions. The deal, based on a €7.4 billion enterprise valuation, strengthens Aramco’s collaboration with Renault Group and Geely, each retaining a 45% stake. This investment aligns with Aramco’s efforts to advance lower-emission mobility solutions, including synthetic fuels and hydrogen.

- In February 2024, Westport Fuel Systems formed a partnership with a global power solutions provider to develop a methanol-based High Pressure Direct Injection (HPDI) fuel system for marine applications. The project, funded by the partner, aims to expand HPDI technology beyond LNG and hydrogen, offering an efficient and cost-effective decarbonization solution.

- In May 2024, ExxonMobil acquired Pioneer Natural Resources, expanding its presence in the Permian Basin. The merger enhances ExxonMobil’s upstream portfolio by doubling its Permian footprint, increasing production capacity, and accelerating net-zero emission targets.

- In December 2024, Phillips 66 and United Airlines signed an agreement to supply sustainable aviation fuel (SAF) at Chicago O’Hare and Los Angeles International Airports. Phillips 66 will initially supply 3 million gallons of SAF, with an option to expand to 8 million gallons by mid-2025. This partnership aligns with efforts to reduce aviation emissions by using low-carbon-intensity fuels from renewable feedstocks.