Photoinitiator Market

Photoinitiator Market Size, Share, Growth & Industry Analysis, By Type (Free Radical, Cationic), By Application (Coatings, Printing, Adhesives, 3D Printing, Others), and Regional Analysis 2024-2031

Pages : 120

Base Year : 2023

Release : October 2024

Report ID: KR1113

Photoinitiator Market Size

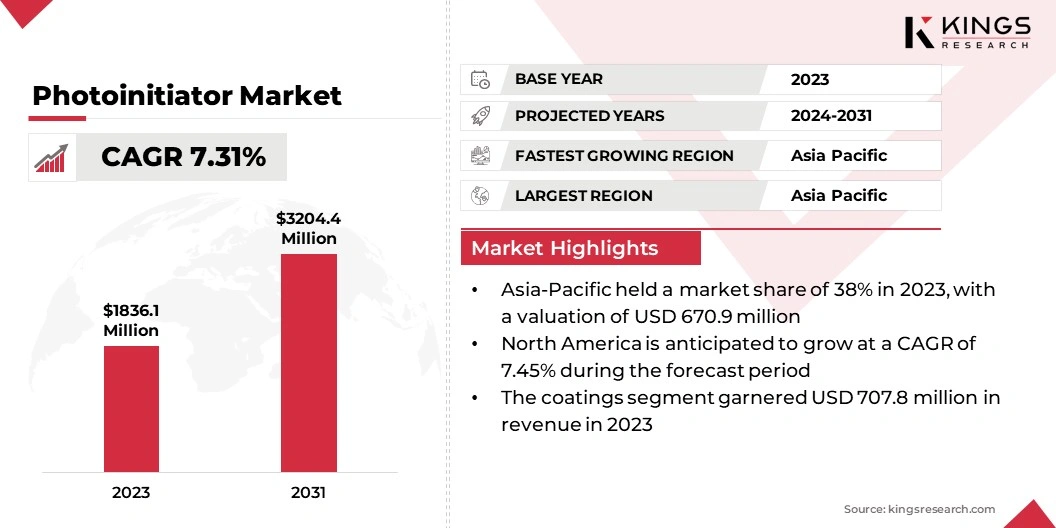

The global Photoinitiator Market size was valued at USD 1,836.1 million in 2023 and is projected to grow from USD 1,956.0 million in 2024 to USD 3,204.4 million by 2031, exhibiting a CAGR of 7.31% during the forecast period. Rising growth of 3D printing applications and surging demand from the packaging industry are driving the growth of the market.

In the scope of work, the report includes services offered by companies such as Merck KGaA, IGM Resins B.V., Arkema, Tokyo Chemical Industry Co., Ltd., DOUBLE BOND CHEMICAL IND. CO., LTD., Eutec Chemical Co., Ltd., JIURI NEW MATERIALS, ADEKA CORPORATION, RAHN AG, Ensince Industry Co., Ltd., and others.

Photopolymerization, a process in which light is used to initiate and propagate a polymerization reaction, is witnessing significant advancements in the biotechnology sector. Photoinitiators play a crucial role in this process by absorbing light and generating reactive species to start polymerization.

In biotechnology, photopolymerization has created new avenues for applications such as tissue engineering, drug delivery systems, and the development of bioactive scaffolds. These advanced materials are engineered to replicate the intricate structures of biological tissues, supporting cell growth and regeneration.

Recent innovations in the development of highly biocompatible photoinitiators have made it easier to use light-based polymerization techniques in medical applications.

For instance, in tissue engineering, photoinitiators are used to create hydrogels that serve as 3D scaffolds for human cell growth, mimicking natural tissues. The non-invasive nature of light-curing techniques further enhance their suitability for sensitive biomedical applications.

A photoinitiator is a chemical compound that, when exposed to light, particularly UV or visible light, initiates a polymerization reaction by generating free radicals or cations. These reactive species facilitate the polymerization of monomers or oligomers, converting them into cross-linked polymers or coatings.

Photoinitiators are essential in UV-curing processes,used across various industries, including coatings, adhesives, printing inks, and 3D printing. Their ability to enable rapid curing at ambient temperatures and with low energy input makes them ideal for applications requiring quick and efficient hardening or drying.

For instance, in the printing industry, photoinitiators are responsible for the fast drying of UV inks, allowing for high-speed production without the need for thermal drying. Additionally, photoinitiators offer excellent control over the curing process, enabling manufacturers to fine-tune the properties of the resulting materials, such as hardness, flexibility, and durability. However, some types of photoinitiators may pose environmental or health risks, leading to increased demand for greener and safer alternatives.

Analyst’s Review

The photoinitiator market is highly competitive, with key companies focusing on strategic innovations, market expansions, and mergers to solidify their positions. Current growth in the market is largely attributed to increasing demand from industries such as coatings, electronics, and 3D printing.

Companies are investing heavily in research and development to enhance their product portfolios, particularly in the areas of eco-friendly and high-performance photoinitiators. This initiative addresses growing regulatory pressures and shifting customer preferences toward sustainable solutions.

Moreover, numerous key players are partnering with end-use industries to co-develop customized photoinitiators that cater to specific applications, including advanced medical devices and automotive coatings.

- In January 2024, iGM Resins initiated legal action to enforce its patents on Omnirad photoinitiators, acquired from BASF in 2016. The globally patented Omnirad 819, a photoinitiator for UV light-triggered radical polymerization of unsaturated resins, is protected by several patents, including EP 1 648 908 B1 and EP 1135 399 B2.

Market expansion into emerging economies has become another strategic imperative, fueled by rapid industrialization and urbanization, which create demand for UV-curable technologies. Despite these positive trends, companies face rising raw material costs and the need for sustainable production practices, compelling them to focus on cost management and operational efficiency.

Photoinitiator Market Growth Factors

The growth of 3D printing is supporting the growth of the market, mainly due to its widespread adoption across industries such as healthcare, automotive, aerospace, and consumer goods. 3D printing, also known as additive manufacturing, depends on precise control of material deposition and curing, with photoinitiators being essential in resin-based techniques such as stereolithography (SLA) and digital light processing (DLP).

These methods utilize light to solidify liquid photopolymer resins layer by layer into solid structures. The versatility of photoinitiators allows manufacturers to produce intricate designs, functional prototypes, and customized products with remarkable precision and speed. With increasing demand for lightweight, strong, and complex components, the use of photoinitiators in 3D printing is rising.

- For instance, in May 2024, Tethon 3D, renowned for its advancements in technical ceramics and 3D printing materials, expanded into bioprinting. This advanced suite features the Bison Bio DLP 3D printer, developed with Carima, along with the Tethon LAP photoinitiator and Tethon GelMA hydrogel bioink, created in collaboration with Cell Bark Innovation. This comprehensive package underscores a significant advancement in bioprinting technology.

This trend is further amplified by innovations in biocompatible materials, which enable applications in medical implants, dental devices, and tissue engineering. As 3D printing technology evolves, photoinitiators is expected to remain critical in ensuring optimal performance and efficiency in the curing process, providing manufacturers with competitive advantages in product quality and production speed.

Stringent regulations regarding the environmental and health impacts of certain photoinitiators present a significant challenge to the development of the photoinitiator market. Governments and regulatory bodies, particularly in regions such as Europe and North America, are increasingly scrutinizing the use of chemicals that pose human risks or harm the environmental.

Some photoinitiators produce harmful byproducts or pose risks during handling and disposal, leading to tighter restrictions on their usage. This regulatory pressure could hinder the growth of the market, as manufacturers face higher compliance costs and potential limitations on the types of photoinitiators they can use.

However, to mitigate this challenge, companies are investing heavily in the development of eco-friendly and low-toxicity alternatives that comply with these regulations. By focusing on research and innovation, they aim to create new generations of photoinitiators that meet stringent safety standards without sacrificing performance. Collaboration with regulatory bodies to ensure compliance and anticipate future policy changes may help manufacturers remain competitive while addressing environmental concerns.

Companies are prioritizing R&D investments in green alternatives, strengthening partnerships with regulators for compliance, and focusing on eco-friendly innovations that meet safety standards to mitigate regulatory challenges and promote growth.

Photoinitiator Market Trends

The expanding applications in the medical device industry is an emerging trend in the photoinitiator market that highlights their versatility and importance in modern healthcare. Photoinitiators are essential in the production of light-cured adhesives, coatings, and materials used in medical devices such as catheters, stents, and dental materials.

Their ability to enable rapid, reliable, and controlled curing makes them indispensable for medical device manufacturers, especially in the production of complex components that require precision and biocompatibility.

- For instance, in August 2024, a review by the National Library of Medicine comprehensively detailed the photoinitiators used in dental materials and hydrogels, covering both natural and synthetic sources. This summary provides valuable insights into the diverse range of photoinitiators and their applications in modern dentistry.

The trend is further supported by the growing demand for disposable medical devices and the increasing use of UV-curable materials in the development of minimally invasive surgical tools and wearable medical devices. In dental applications, photoinitiators are key for creating high-quality, durable restorations such as fillings, crowns, and veneers.

This expansion in medical applications is fueled by innovations in biocompatible and non-toxic photoinitiators, which ensure that these materials are safe for human use. As the healthcare industry advances, the demand for specialized photoinitiators in medical devices is anticipated to grow, creating significant opportunities for manufacturers.

Segmentation Analysis

The global market has been segmented based on type, application, and geography.

By Type

Based on type, the market is segmented into free radical and cationic. The free radical segment captured the largest share of 58.23% in 2023. This expansion is largely attributed to the widespread use of free radical photoinitiators in various UV-curable applications. Free radical photoinitiators are versatile, highly effective, and suitable for a broad range of materials, making them a highly preferred choice for industries such as coatings, adhesives, and inks.

These photoinitiators operate by generating free radicals upon exposure to UV or visible light, which subsequently trigger the polymerization of monomers and oligomers, leading to fast and efficient curing. Free radical photoinitiators are popular due to their compatibility with various formulations, especially in industries requiring fast production cycles and high throughputs, such as automotive coatings, packaging, and electronics.

Furthermore, these photoinitiators offer a balance of performance and cost-effectiveness, appealing to manufacturers seeking to optimize production efficiency. The ongoing advancements in UV-curing technologies and the expanding applications of free radical polymerization further contribute to the lgrowth of the segment.

By Application

Based on application, the market has been classified into coatings, printing, adhesives, 3d printing, and others. The coatings segment led the photoinitiator market in 2023, reaching a valuation of USD 707.8 million, mainly due to the growing demand for UV-curable coatings across various industries, including automotive, electronics, packaging, and furniture.

UV-curable coatings, which utilize photoinitiators to initiate polymerization, offer significant advantages such as faster curing times, lower energy consumption, and enhanced product performance compared to traditional coatings. These factors are particularly advantageous in high-volume production environments where speed and efficiency are critical.

The coatings segment has seen significant growth, as a result of increasing regulatory pressure to reduce volatile organic compounds (VOCs) and emissions associated with conventional coatings. UV-curable coatings, which are free of solvents and VOCs, present an eco-friendly alternative, aligning with the sustainability goals of both manufacturers and consumers.

Additionally, the development of more durable, scratch-resistant, and aesthetically pleasing coatings has boosted demand, especially in the automotive and consumer electronics industries, where surface quality is essential. The versatility of UV coatings, coupled with advancements in photoinitiator technology, is bolstering the growth of the coatings segment.

Photoinitiator Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia Pacific, MEA, and Latin America.

Asia-Pacific photoinitiator market held a subatantial share of 38% and was valued at USD 670.9 million in 2023. Thiss dominance is mainly propelled by the rapid industrialization and urbanization in major economies such as China, Japan, South Korea, and India. These countries have witnessed a surge in demand for UV-curable products, particularly in industries the automotive, electronics, and packaging industries, where photoinitiators crucial for efficient and high-speed production processes.

China, a major manufacturing hub, contributes significantly to this growth through its expanding use of photoinitiators in coatings, adhesives, and printing inks. Moreover, government policies promoting the adoption of eco-friendly technologies have fueled the demand for UV-curable materials.

In addition, the increasing investment in infrastructure development and the growing middle-class population are boosting the demand for consumer goods and packaging solutions, highlighting the need for UV-curable technologies in the Asia-Pacific as a lucrative market for market.

North America photoinitiator market is projected to grow at a significant CAGR of 7.45% in the forthcoming years, stimulated by the increasing adoption of UV-curing technologies across multiple industries. This growth is largely due to the rising demand for sustainable and energy-efficient solutions in sectors such as automotive, electronics, and healthcare.

In the automotive industry, for instance, photoinitiators are essential in producing durable coatings and adhesives that contribute to vehicle longevity and performance. Additionally, North America’s well-established electronics and semiconductor industries rely on photoinitiators for high-precision applications, such as circuit board manufacturing and UV-curable resins.

Moreover, the region’s stringent environmental regulations aimed at reducing emissions and harmful chemicals, have fostered the adoption of eco-friendly UV-curable materials, thereby boosting regional market growth.

As companies increasingly invest in research and development to create high-performance, low-toxicity photoinitiators, North America is poised to become a key growth region, with substantial opportunities for innovation and expansion.

Competitive Landscape

The global photoinitiator market report will provide valuable insights with a specialized emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies, such as partnerships, mergers and acquisitions, product innovations, and joint ventures, to expand their product portfolio and increase their market shares across different regions.

Companies are implementing impactful strategic initiatives, such as expansion of services, investments in research and development (R&D), establishment of new service delivery centers, and optimization of their service delivery processes, which are likely to create new opportunities for market growth.

List of Key Companies in Photoinitiator Market

- Merck KGaA

- IGM Resins B.V.

- Arkema

- Tokyo Chemical Industry Co., Ltd.

- DOUBLE BOND CHEMICAL IND. CO., LTD.

- Eutec Chemical Co., Ltd.

- JIURI NEW MATERIALS

- ADEKA CORPORATION

- RAHN AG

- Ensince Industry Co., Ltd.

Key Industry Developments

- January 2023 (Launch): Everlight Chemical launched an innovative, water-based photoinitiator, expanding its portfolio of sustainable chemical solutions. This product addresses the growing demand for eco-friendly options while ensuring both high performance and reduced environmental impact.

The global photoinitiator market is segmented as:

By Type

- Free Radical

- Cationic

By Application

- Coatings

- Printing

- Adhesives

- 3D Printing

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- France

- UK

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

CHOOSE LICENCE TYPE

.webp)

Frequently Asked Questions (FAQ's)

Get the latest!

Get actionable strategies to empower your business and market domination

- Deliver Revenue Impact

- Demand Supply Patterns

- Market Estimation

- Real-Time Insights

- Market Intelligence

- Lucrative Growth Opportunities

- Micro & Macro Economic Factors

- Futuristic Market Solutions

- Revenue-Driven Results

- Innovative Thought Leadership