Semiconductor and Electronics

Power Semiconductor Market

Power Semiconductor Market Size, Share, Growth & Industry Analysis, By Product (Silicon Carbide, Gallium Nitride, Others), By Component (Discrete, Module, Power Integrated Circuits), By Application (IT & Telecommunication, Consumer Electronics, Automotive & Others), and Regional Analysis, 2024-2031

Pages : 120

Base Year : 2023

Release : August 2024

Report ID: KR1019

Power Semiconductor Market Size

The global Power Semiconductor Market size was valued at USD 48.93 billion in 2023 and is projected to grow from USD 51.03 billion in 2024 to USD 76.57 billion by 2031, exhibiting a CAGR of 5.97% during the forecast period. The market is expanding rapidly, driven by increased adoption of renewable energy sources and advancements in high-efficiency technologies.

The demand for power semiconductors is rising as industries seek more effective power management solutions and improved system performance. Innovations, such as advanced cooling technologies and integration with digital systems, are enhancing the capabilities of power semiconductors, contributing to robust market growth.

In the scope of work, the report includes solutions offered by companies such as Infineon Technologies AG, Texas Instruments Inc., Qorvo Inc., STMicroelectronics, NXP Semiconductors., Semiconductor Components Industries, LLC, Renesas Electronics Corporation, Broadcom, Toshiba Corporation, Fuji Electric Co. Ltd, and others.

The power semiconductor market is experiencing robust growth, driven by increasing demand across various industries such as automotive, renewable energy, and industrial applications. The rise of electric vehicles along with the global shift toward renewable energy sources is significantly boosting the need for efficient power management solutions.

- For instance, a recent report from the International Energy Agency revealed that electric car markets experienced robust growth with sales of EVs reaching nearly 14 million in 2023. The market share of electric vehicles surged from around 4% in 2020 to a staggering 18% in 2023, reflecting a significant shift in consumer preferences toward more sustainable transportation options.

Advanced technologies like wide bandgap (WBG) semiconductors, including silicon carbide (SiC) and gallium nitride (GaN), are revolutionizing power semiconductors by offering superior performance. Government incentives for clean energy and stringent emission regulations further drive market growth.

Power semiconductors are critical components in the management and conversion of electrical power across various applications. They are engineered to handle high voltages and currents efficiently, ensuring optimal performance and energy efficiency in power supplies, motor drives, and renewable energy systems.

Key devices in this category include diodes, transistors, and thyristors, each tailored for specific roles in power regulation and conversion. By improving energy efficiency and system reliability, power semiconductors play a pivotal role in modern electronics, impacting sectors from consumer electronics and industrial machinery to electric vehicles.

Analyst’s Review

Strategic partnerships between major semiconductor and electronics companies are driving advancements in power semiconductors. By combining expertise and resources, these collaborations focus on developing innovative solutions like cost-efficient, high-performance onboard chargers.

- For instance, in June 2024, Texas Instruments, a US semiconductor company, and Delta Electronics, a Taiwanese electronics firm, partnered to advance power semiconductors for electric vehicles. Their initial effort was to develop a lighter and more cost-effective 11 kW onboard charger. This collaboration was just the start of the next big leap, with both companies planning to use their joint innovation lab in Pingzhen, Taiwan. Their long-term goal is to enhance power density, boost performance, and reduce component size, aiming to accelerate the launch of safer, more efficient, and affordable electric vehicles.

Such initiatives aim to enhance power density, reduce component size, and improve overall performance. These collaborative efforts may contribute significantly to market growth by revolutionizing technology and meeting the evolving demands of the electric vehicle segment, thereby fostering market growth in the coming years.

Power Semiconductor Market Growth Factors

The rise in electric vehicle (EV) adoption is propelling the power semiconductor market. As EVs become more prevalent, there is a growing need for advanced power semiconductor devices to efficiently manage their electric power systems.

- According to the International Energy Agency (IEA), in the first quarter alone in 2024, global sales of electric cars exceeded 3 million, representing a 25% increase compared to 2023. It is anticipated that around 17 million electric vehicles will be sold by the end of 2024, marking a notable year-on-year rise of over 20%. This growth is expected to accelerate further in the latter half of the year.

These systems include critical components, such as inverters, converters, and battery management systems, which are increasingly relying on power semiconductors for optimal performance. The global push toward sustainable transportation and implementing stringent emissions regulations further fuel this demand.

Governments and consumers are increasingly prioritizing eco-friendly alternatives, which is leading to substantial market growth for power semiconductors. A significant challenge in the power semiconductors market is the high cost of advanced semiconductor materials and manufacturing processes.

The complexity and expense of producing cutting-edge materials like silicon carbide (SiC) and gallium nitride (GaN) can restrict the widespread adoption of power semiconductors, particularly among smaller companies and in cost-sensitive applications. This high-cost barrier impedes market growth by limiting the accessibility and scalability of these technologies. To address this issue, key players invest in research and development to enhance manufacturing efficiencies and reduce costs.

- For instance, in June 2024, Infineon Technologies AG introduced the CoolGaN Transistor 700 V G4 product family, which offers a 20% improvement in performance over other GaN products, reduces power losses, and provides cost-effective solutions.

Companies are exploring opportunities to lower production costs and make advanced power semiconductors more accessible by focusing on technological advancements, forming strategic partnerships, and optimizing manufacturing processes, thus accelerating market adoption.

Power Semiconductor Industry Trends

The global shift toward renewable energy sources, such as wind and solar power, propels the demand for power semiconductors. These devices are crucial in converting and managing power within renewable energy systems, ensuring efficient energy generation and distribution.

As renewable energy becomes more mainstream, the need for reliable and efficient power semiconductors is growing. Government incentives and policies promoting clean energy are further enhancing the adoption of these semiconductors, making them essential components in various renewable energy applications and thereby fostering market expansion.

There is a growing trend toward the development and adoption of wide bandgap (WBG) semiconductors, such as silicon carbide (SiC) and gallium nitride (GaN). These advanced materials offer significantly superior performance compared to traditional silicon-based semiconductors, including faster switching speeds, higher efficiency, and better thermal conductivity.

As a result, WBG semiconductors are increasingly being used in high-power and high-frequency applications, revolutionizing the field of power semiconductors. Their ability to handle higher voltages and temperatures with greater efficiency makes them an ideal choice for use in electric vehicles, renewable energy systems, and industrial equipment. This shift toward WBG semiconductors drives innovation and growth in the power semiconductor industry.

Segmentation Analysis

The global market has been segmented based on product, component, application, and geography.

By Product

Based on product, the power semiconductor market has been categorized into silicon carbide, gallium nitride, and others. The silicon carbide segment garnered the highest revenue of USD 18.26 billion in 2023, fueled by its superior performance over traditional silicon semiconductors. SiC's high efficiency at elevated temperatures, voltages, and frequencies makes it ideal for applications in electric vehicles (EVs) and renewable energy systems.

The automotive industry drives demand for SiC due to its benefits in powertrains and charging systems, while the renewable energy sector values its efficiency in power conversion. Technological advancements are lowering costs and enhancing performance, while supportive government policies are accelerating adoption, thereby fostering segmental growth based on product.

By Component

Based on component, the market has been categorized into discrete, module, and power integrated circuits. The discrete segment captured the largest power semiconductor market share of 53.40% in 2023. This segment includes components, such as diodes, transistors, and thyristors, which are crucial for regulating power in consumer electronics, automotive systems, and industrial machinery.

The increasing demand for efficient and reliable power solutions in electronic devices, electric vehicles, and automation systems is driving further market expansion. Technological advancements enhance the performance and efficiency of discrete components while their cost-effectiveness ensures widespread adoption in diverse applications.

By Application

Based on application, the market has been categorized into IT & telecommunication, consumer electronics, automotive, aerospace & defense, transportation, and others. The consumer electronics segment is expected to garner the highest revenue of USD 26.80 billion by 2031, which is mainly driven by the rising demand for advanced electronic devices, such as smartphones, tablets, laptops, and home appliances.

Power semiconductors play a critical role in these devices, ensuring efficient power management and reliable performance. The proliferation of smart gadgets, increasing consumer preference for high-performance electronics, and the shift towards energy-efficient technologies are propelling market expansion.

Technological advancements enhance semiconductor efficiency and miniaturization, meeting the growing need for compact and high-functioning devices. This growth is further supported by innovation in power management solutions and increasing integration of electronics in everyday consumer products.

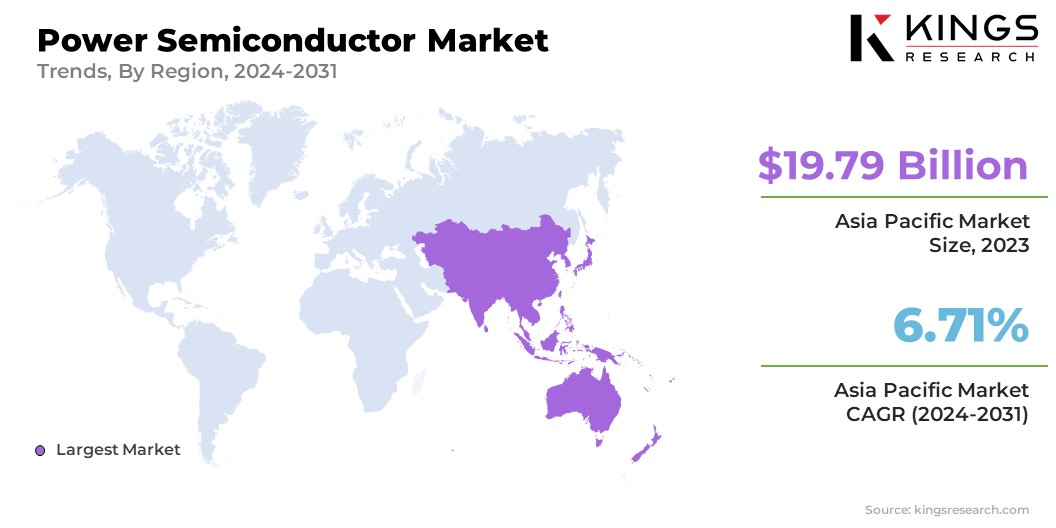

Power Semiconductor Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

Asia-Pacific power semiconductor market share stood around 40.44% in 2023 in the global market, with a valuation of USD 19.79 billion. Key factors contributing to this growth include a booming automotive industry, rising adoption of renewable energy sources, and expanding consumer electronics markets.

The region is also witnessing significant investments in smart technologies and infrastructure development, which further propels the demand for advanced power management solutions. In China, the power semiconductors market is experiencing notable expansion, bolstered by its status as the world's largest vehicle market, leading in annual sales and manufacturing output.

- According to the Global System for Mobile Communications Association, by 2025, China is expected to produce approximately 35 million vehicles domestically. The country's ambitious goal of achieving carbon neutrality by 2060 is driving the demand for power semiconductors, particularly within the electric vehicle (EV) sector. This proactive approach, combined with a strong push towards sustainable energy solutions is further expected to contribute to the market growth in the region.

North America is anticipated to witness significant growth at a CAGR of 6.20% over the forecast period. Notable investments in smart grid technologies and renewable energy infrastructure are further boosting the need for efficient power semiconductors. In addition, North America’s focus on research and development is fostering innovation in semiconductor technologies.

- According to the US Congressional Budget Office, defense spending in the U.S. is estimated to rise annually through 2033, with outlays rising from USD 746 billion in 2023 to an estimated USD 1.1 trillion by 2033. This expenditure is expected to account for 6% of the country's GDP in 2024, up from 3.9% in 2023 and 2.7% in 2021.

Therefore, the expanding defense budgets are anticipated to provide significant growth opportunities for the power semiconductors market, as increased defense spending drives demand for advanced electronic systems and components.

Competitive Landscape

The global power semiconductor market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies, such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Companies are implementing impactful strategic initiatives, such as expanding services, investing in research and development (R&D), establishing new service delivery centers, and optimizing their service delivery processes, which are likely to create new opportunities for market growth.

List of Key Companies in the Power Semiconductor Market

- Infineon Technologies AG

- Texas Instruments Inc.

- Qorvo Inc.

- STMicroelectronics

- NXP Semiconductors.

- Semiconductor Components Industries, LLC

- Renesas Electronics Corporation

- Broadcom

- Toshiba Corporation

- Fuji Electric Co. Ltd

Key Industry Development

- April 2024 (Partnership): Infineon Technologies AG partnered with FOXESS, a leading company in the green energy sector, to supply its power semiconductor devices. Infineon provided FOXESS with CoolSiC MOSFETs 1200 V for use with EiceDRIVER gate drivers in industrial energy storage applications. In addition, FOXESS' string PV inverters incorporated Infineon's IGBT7 H7 1200 V power semiconductor devices. This collaboration was aimed to advance the development of green energy solutions.

The global power semiconductor market has been segmented:

By Product

- Silicon Carbide

- Gallium Nitride

- Others

By Component

- Discrete

- Module

- Power Integrated Circuits

By Application

- IT & Telecommunication

- Consumer Electronics

- Automotive

- Aerospace & Defense

- Transportation

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- France

- UK

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

CHOOSE LICENCE TYPE

Frequently Asked Questions (FAQ's)

Get the latest!

Get actionable strategies to empower your business and market domination

- Deliver Revenue Impact

- Demand Supply Patterns

- Market Estimation

- Real-Time Insights

- Market Intelligence

- Lucrative Growth Opportunities

- Micro & Macro Economic Factors

- Futuristic Market Solutions

- Revenue-Driven Results

- Innovative Thought Leadership