ICT-IOT

Substation Automation Market

Substation Automation Market Size, Share, Growth & Industry Analysis, By Component (Hardware, Software, Service), By Type (Transmission Substation, Distribution Substation), By Technology (New, Retrofit), By End Use, and Regional Analysis, 2024-2031

Pages : 190

Base Year : 2023

Release : April 2025

Report ID: KR1698

Market Definition

The market encompasses technologies and systems that enable real-time monitoring, control, and protection of electrical substations using Intelligent Electronic Devices (IEDs), Supervisory Control and Data Acquisition (SCADA) systems, and communication networks.

It involves processes such as data acquisition, fault detection, and automated switching to enhance grid efficiency and reliability. The market focuses on the formulation of digital substations, advanced protection schemes, and cybersecurity measures.

Substation automation is widely used in power transmission networks, industrial plants, and renewable energy integration, ensuring operational efficiency, reduced downtime, and enhanced grid resilience through automation, remote operation, and predictive maintenance solutions.

Substation Automation Market Overview

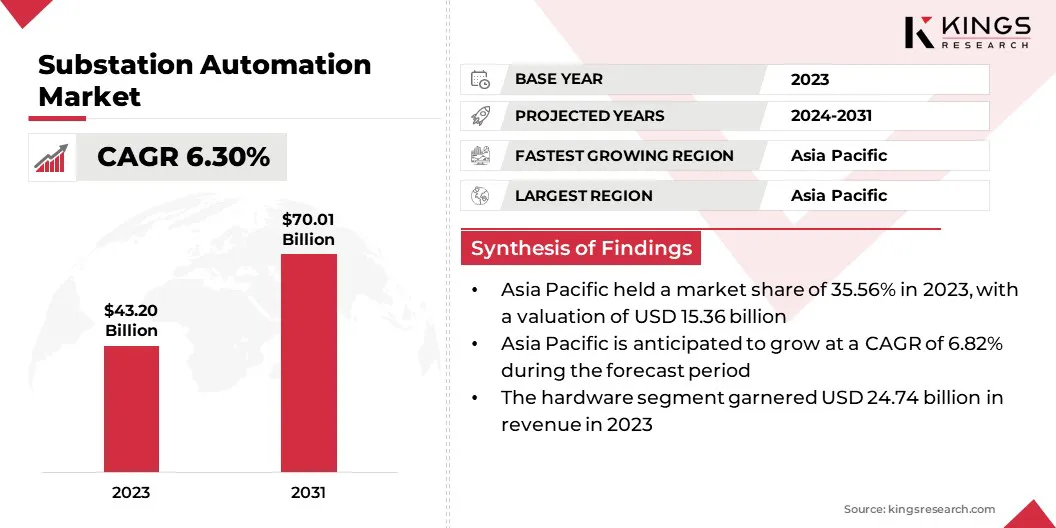

The global substation automation market size was valued at USD 43.2 billion in 2023 and is projected to grow from USD 45.65 billion in 2024 to USD 70.01 billion by 2031, exhibiting a CAGR of 6.30% during the forecast period.

The market is driven by increasing investments in grid modernization and the integration of renewable energy sources. Utilities are adopting advanced digital solutions to enhance grid reliability, efficiency, and security.

Additionally, the rising focus on cybersecurity in energy infrastructure is accelerating the deployment of automation technologies, ensuring secure and resilient power distribution systems in response to evolving threats and regulatory requirements.

Major companies operating in the substation automation industry are ABB, Schneider Electric SE, Siemens, General Electric, Hitachi Energy Ltd., Yokogawa Electric Corporation, Rockwell Automation, Inc., Cisco, Schweitzer Engineering Laboratories, Inc., Eaton, Mitsubishi Electric Corporation, Honeywell International Inc., Trilliant Holdings Inc., Alstom SA, and S&C Electric Company.

The growing shift toward smart grids is driving the market. Utilities are adopting automation technologies to enable real-time monitoring, data-driven decision-making, and improved operational efficiency.

Smart grids require advanced automation solutions to enhance power distribution, optimize load management, and ensure uninterrupted electricity supply. Governments and regulatory bodies are investing in smart grid projects, further accelerating the deployment of substation automation solutions to modernize energy infrastructure and enhance overall grid performance.

- At the end of 2022, the European Commission introduced the EU action plan, "Digitalisation of the Energy System." The Commission estimates that approximately EUR 584 billion (USD 633 billion) will be invested in the European electricity grid by 2030. Out of this, EUR 170 billion (USD 184 billion) is expected to be allocated for digitalisation, including smart meters, automated grid management, digital metering technologies, and enhancements in field operations.

Key Highlights:

- The substation automation industry size was valued at USD 43.2 billion in 2023.

- The market is projected to grow at a CAGR of 6.30% from 2024 to 2031.

- Asia Pacific held a market share of 35.21% in 2023, with a valuation of USD 15.36 billion.

- The hardware segment garnered USD 24.74 billion in revenue in 2023.

- The transmission substation segment is expected to reach USD 40.83 billion by 2031.

- The new segment secured the largest revenue share of xx% in 2023.

- The utilities segment is poised for a robust CAGR of xx% through the forecast period.

- The market in North America is anticipated to grow at a CAGR of 6.43% during the forecast period.

Market Driver

"Adoption of Digital Substations"

The shift from traditional substations to digital substations is accelerating the growth of the substation automation market. Digital substations replace conventional copper wiring with fiber-optic communication, enhancing reliability and reducing operational costs.

Digital substations improve real-time monitoring, asset management, and fault detection, enhancing power system efficiency. Utilities and industrial operators are increasingly adopting digital solutions to improve operational resilience, minimize maintenance costs, and enhance the flexibility of energy networks in response to evolving power demands.

- In February 2024, GE Vernova’s Grid Solutions business introduced GridBeats, a suite of software-defined automation solutions designed to accelerate grid digitalization and improve grid resilience. GridBeats offers functionalities for substation digitalization, autonomous grid zone management, and remote monitoring of devices and communication networks.

Market Challenge

"Cybersecurity Risks in Substation Automation"

A significant challenge in the growth of the substation automation market is the increasing risk of cyber threats targeting critical power infrastructure. Such vulnerabilities to cyberattacks pose a serious threat to grid stability and security as substations become more digitalized and interconnected.

Companies are implementing advanced cybersecurity solutions, including encryption, multi-layered authentication, and intrusion detection systems. Compliance with regulatory cybersecurity frameworks such as NERC CIP and IEC 62443 is also being prioritized. Additionally, organizations are investing in AI-driven threat detection and real-time monitoring to enhance resilience against evolving cyber threats.

Market Trend

"Modernization of Aging Power Infrastructure"

Governments and utilities are investing in automation technologies to extend the lifespan of existing infrastructure while minimizing downtime. The integration of advanced monitoring systems enables predictive maintenance, reducing unplanned outages.

Automated substations play a critical role in ensuring a stable electricity supply, supporting economic growth and meeting the increasing demand for efficient power distribution.

- In March 2025, the parliament of Germany approved a USD 544 billion special fund to support infrastructure modernization, defense, and climate action. This fund, to be deployed over 12 years, aims to upgrade critical systems, including energy grids and transport networks, while reducing industrial and structural emissions.

Substation Automation Market Report Snapshot

|

Segmentation |

Details |

|

By Component |

Hardware, Software, Service |

|

By Type |

Transmission Substation, Distribution Substation |

|

By Technology |

New, Retrofit |

|

By End Use |

Utilities, Steel, Oil & Gas, Mining, Transportation, Others |

|

By Region |

North America: U.S., Canada, Mexico |

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe |

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific |

|

|

Middle East & Africa: Turkey, UAE, Saudi Arabia, South Africa, Rest of Middle East & Africa |

|

|

South America: Brazil, Argentina, Rest of South America |

Market Segmentation:

- By Component (Hardware, Software, Service): The hardware segment earned USD 24.74 billion in 2023, due to the high demand for intelligent electronic devices (IEDs), process interface units, and communication hardware, which are essential for real-time data processing, grid reliability, and seamless automation integration.

- By Type (Transmission Substation, Distribution Substation): The transmission substation segment held 59.32% share of the market in 2023, due to the increasing demand for grid modernization, higher voltage handling capacity, and the critical role of automation in ensuring efficient long-distance power transmission and integration of renewable energy sources.

- By Technology (New, Retrofit): The new segment is projected to reach USD 43.43 billion by 2031, owing to its ability to enhance grid efficiency, interoperability, and real-time monitoring, aligning with increasing investments in smart grid infrastructure and the growing demand for advanced digital solutions.

- By End Use (Utilities, Steel, Oil & Gas, Mining, Transportation, Others): The utilities segment is poised for significant growth at a CAGR of 6.64% through the forecast period, due to the large-scale deployment of automated substations for grid modernization, reliability enhancement, and seamless integration of renewable energy sources to meet rising electricity demand efficiently.

Substation Automation Market Regional Analysis

Based on region, the market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

Asia Pacific accounted substation automation market share stood around 35.21% in 2023, with a valuation of USD 15.36 billion. The market in the region is registering rapid growth, due to large-scale investments in power infrastructure by governments in China, India, Indonesia, Vietnam, and the Philippines.

Expanding industrial zones, urban developments, and electrification of rural areas require modernized substations with automation, remote monitoring, and real-time data analytics.

National initiatives such as China’s Belt and Road Initiative (BRI) and India’s Revamped Distribution Sector Scheme (RDSS) are accelerating the deployment of automated substations to ensure efficient and reliable power transmission.

Furthermore, countries like Japan, South Korea, China, and Singapore are leading in smart manufacturing and Industry 4.0, driving the demand for automated power substations. With manufacturing hubs integrating AI, IoT, and cloud computing, automated substations help optimize power usage, reduce downtime, and enhance operational resilience.

The substation automation industry in North America is poised for significant growth at a robust CAGR of 6.43% over the forecast period. The market is fueled by the demand for cyber-secure digital substations that enhance grid reliability and data security in the region.

North America’s critical power infrastructure is increasingly vulnerable to cyberattacks, prompting utilities to integrate secure substation automation technologies. Additionally, the increasing adoption of IoT, AI, and cloud-based analytics is reshaping the market in North America.

Smart grid initiatives encourage the deployment of digital substations equipped with intelligent sensors, automated switching systems, and remote diagnostics. 5G connectivity and edge computing are further improving real-time grid monitoring, predictive maintenance, and fault detection, driving substantial investments in automated substation solutions.

Regulatory Frameworks

- In the U.S., The market is regulated by multiple authorities ensuring grid reliability, safety, and cybersecurity. The National Electrical Safety Code (NESC) sets installation and operational safety standards for substations, while the Federal Energy Regulatory Commission (FERC) and the North American Electric Reliability Corporation (NERC) establish and enforce bulk power system reliability standards. NERC’s Critical Infrastructure Protection (CIP) standards play a crucial role in securing substation automation systems against cyber threats.

- The EU's regulatory framework for substation automation is based on IEC 61850, ensuring interoperability and communication standardization across member states. The European Network of Transmission System Operators for Electricity (ENTSO-E) sets grid operation standards, including those for digital substations. Additionally, IEC 60364 governs electrical installations, providing consistency in safety measures. EU initiatives such as Digitalisation of Energy Action Plan aim to enhance automation and smart grid deployment across Europe.

- Japan regulates substation automation through the Japan Electric Association (JEA) Standards, ensuring safe and efficient electrical installations. The government’s Energy Conservation Act promotes the modernization of substations as part of its smart grid strategy. Utilities such as Tokyo Electric Power Company (TEPCO) invest in substation digitalization to enhance grid resilience, particularly in disaster-prone areas. Automation and remote monitoring are key components of Japan’s initiative to improve power stability.

Competitive Landscape:

The substation automation industry is characterized by market players that are actively adopting strategies focused on advancements in digital substation technology to enhance grid efficiency, reliability, and automation.

By integrating next-generation process interface units and modular digital solutions, companies are streamlining substation operations, reducing infrastructure complexity, and improving interoperability.

These innovations are accelerating the shift toward fully digital substations, reinforcing their role in modern grid infrastructure. As a result, such strategic advancements are significantly contributing to the growth of the market.

- In January 2024, Hitachi Energy enhanced its cutting-edge digital substation technology with the introduction of SAM600 3.0, an advanced process interface unit (PIU) designed to accelerate the transition to digital substations for transmission utilities. The newly developed, modular SAM600 integrates three functionalities into a single device, allowing it to function as a merging unit, a switchgear control unit, or a hybrid of both. This versatile design supports multiple installation configurations, enhancing flexibility and efficiency in substation automation.

List of Key Companies in Substation Automation Market:

- ABB

- Schneider Electric SE

- Siemens

- General Electric

- Hitachi Energy Ltd.

- Yokogawa Electric Corporation

- Rockwell Automation, Inc.

- Cisco

- Schweitzer Engineering Laboratories, Inc.

- Eaton

- Mitsubishi Electric Corporation

- Honeywell International Inc.

- Trilliant Holdings Inc.

- Alstom SA

- S&C Electric Company

Recent Developments (Expansion/Product Launch)

- In July 2024, GE Vernova announced plans to provide GE Algeria Turbines (GEAT) with high-voltage equipment, components, and grid automation solutions for 134 substations by 2028 to strengthen Algeria’s grid infrastructure. The supplied technology is set to play a key role in integrating renewable energy sources while ensuring a stable and reliable power supply to support the country’s expanding population and economic growth.

- In March 2023, Honeywell launched its Versatilis Transmitters for condition-based monitoring of rotating equipment, including pumps, motors, compressors, fans, blowers, and gearboxes. These transmitters offer critical measurements that enhance safety, availability, and reliability across various industries. It extends to applications such as improving heat exchange efficiency and ensuring the reliability of substations, further optimizing industrial operations.

CHOOSE LICENCE TYPE

Frequently Asked Questions (FAQ's)

Get the latest!

Get actionable strategies to empower your business and market domination

- Deliver Revenue Impact

- Demand Supply Patterns

- Market Estimation

- Real-Time Insights

- Market Intelligence

- Lucrative Growth Opportunities

- Micro & Macro Economic Factors

- Futuristic Market Solutions

- Revenue-Driven Results

- Innovative Thought Leadership